Crypto Bulls Take a Breath as Bitcoin, XRP Prices Dip

Prices are down a bit nearly across the board in crypto today. But only a little, and all signs point to the bull run being far from over.

The Bitcoin bull run has been frantic. Taking a moment to breathe probably isn’t a bad idea.

Total market capitalization for crypto has increased by $100 billion in the last 48 hours. Today, though, that excitement has been tempered somewhat.

Bitcoin is down a little more than half a percent, settling around $22,600. XRP, the third largest cryptocurrency by market cap, took the biggest hit, down nearly 12% and trading just above $0.50.

Bitcoin still bullish

Although Bitcoin is currently in uncharted territory after setting a new all-time high and breaking through the psychological barrier of $23,000, the cryptocurrency is once again returning to calm waters.

Bitcoin almost hit the $24,000 milestone, but has since pulled back a bit. It got as low as $22,329 today before settling into its current price.

But even with this minor slide, Bitcoin remains bullish. It’s relative strength index (a metric that measures demand among buyers and sellers) suggests there’s still a strong appetite for the crypto asset.

The Crypto Fear and Greed Index confirms this sentiment, showing that there's extreme greed in the markets, with greediness among traders currently at 95 on a scale of 1 to 100.

Holders are likely hoping they stay greedy.

XRP crashed, but it could be much worse

Meanwhile, Ripple’s XRP suffered a relatively significant drop in price today following a huge upswing earlier this month.

As noted previously, the Flare Network Spark airdrop, which promised free crypto to anyone holding XRP at an eligible exchange, led to renewed excitement around the third-most popular crypto.

Since then, though, the token recovered, and jumped from $0.46 to $0.66, right around the time Bitcoin reached its new all-time high price.

Unlike Bitcoin, however, it hasn’t succeeded in maintaining that momentum. Still, even at just $0.57 per coin, that’s still 194% more than XRP was worth at the start of the year.

What Will Bitcoin Technology Look Like in 20 Years?

Bitcoin has evolved hugely in its decade-plus lifespan—but what does the far future hold for the cryptocurrency's underlying technologies?

In brief

Bitcoin's decentralized nature throws up some challenges to upgrading its technology.

Two of its biggest challenges include scalability and the possibility of introducing smart contracts to the Bitcoin blockchain.

One success case for BTC in 20 years would see it becoming the global open settlement layer for DeFi services and the IoT economy.

Since its inception over a decade ago, Bitcoin has grown from an obscure curiosity for IT geeks to a worldwide phenomenon, revolutionizing the global financial industry in the process. During this time, its network has evolved to keep up with the times—but what changes could be wrought on the underlying technology of Bitcoin technology in the next decade or two?

And, more importantly, does Bitcoin really need to change?

Some assembly required

Even today, Bitcoin demands a certain level of computer literacy from its holders. But when the cryptocurrency was first introduced to the world over a decade ago, it was even less user-friendly. Since then, several useful improvements—such as Segregated Witness (SegWit) and Lightning Network, a second-level scalability solution—have been proposed and successfully implemented, although this process was far from simple.

According to Dmytro Volkov, chief technology officer at crypto exchange CEX.IO, Bitcoin’s very own decentralized nature is both a blessing and a curse. On one hand, the absence of any controlling entity makes Bitcoin truly decentralized and community-driven. On the other, it makes it much harder to upgrade.

"It requires a great deal of effort to reach consensus on implementing big changes to the blockchain code."

Dmytro Volkov

“There is an open-source community and development, but it requires a great deal of effort to reach consensus on implementing big changes to the blockchain code. A good example was SegWit, which took a lot of time and effort to implement,” Volkov told Decrypt.

He added that this may be perceived as Bitcoin’s weakness in comparison with other blockchain projects such as Ethereum—which has a native team, author, and community leader, “all of which make complex large-scale changes to Ethereum relatively easy and quick, with high levels of consensus.”

“On the other hand, we can see it as a strength of Bitcoin because it offers maximum decentralization in terms of changing the blockchain’s code: changes require truly worldwide consensus, which ensures that only the most wanted features will be added, in the most secure way,” Volkov explained.

Thus, while Bitcoin’s architecture makes the blockchain more conservative and narrower in functionality, it also makes it more simple, secure, and reliable, he added.

What are Bitcoin’s biggest challenges today?

Speaking to Decrypt, Muneeb Ali, founder and CEO of Blockstack, an open-source network for decentralized applications (dapps) and smart contracts, outlined two main challenges that Bitcoin is facing today. First, for it to become the universal reserve currency, Bitcoin must be able to scale to hundreds of millions—or even billions—of transactions. Second, there needs to be a way to safely introduce smart contracts on the blockchain.

“For scalability, it’s pretty clear at this point that the base blockchain is not where you do hundreds of millions of transactions. Higher layers or sidechains will take on that load and settle back on Bitcoin,” Ali explained to Decrypt.

He added that there are several technical directions currently being explored such as Lightning channels, sidechains like Liquid, connected chains like Stacks, and even zero knowledge proof-based solutions that allow condensing a lot of data while keeping it provable.

“For smart contracts, introducing them on sidechains (like Liquid with Simplicity Lang), merged mined chains (like RSK with Solidity), and connected chains (like Stacks with Clarity Lang) seems to be the way to go,” Ali added.

He also highlighted experimental solutions such as Sapio that are trying to implement multi-step smart contracts on the base layer of Bitcoin.

“I think that significant progress on both fronts can be made within the next 1–3 years,” Ali suggested.

Still not ready for prime time

However, most experts interviewed by Decrypt agreed that many innovative Bitcoin solutions are still in the early stages of their development and are far from ready for mass adoption.

Layer two solutions such as Lightning and Liquid are technically interesting and have potential, said Antonis Polemitis, blockchain specialist and the University of Nicosia CEO. But both are "rather experimental technically and are still working on product-market fit,” he added.

“Unlike Layer one, that can plausibly say that it is a low transaction volume solution, optimized for decentralization, success at layer two would mean high volume. And there are other even earlier stage technologies, like Taproot,” he told Decrypt.

While Bitcoin will likely play a leading role as a long-term value storage method in the cryptocurrency world, it is still relatively slow and has low throughput—and will likely remain this way due to how hard it is to upgrade the blockchain, added Volkov.

“SegWit was a big change to the Bitcoin blockchain, but it didn’t solve the low throughput problem. Lightning didn’t solve the throughput problem either, because it is not easy to use and there are plenty of other alternatives on other blockchains to accomplish the same thing easily,” he explained.

Thus, other blockchains are likely to surpass Bitcoin in terms of speed and throughput (which are crucial for day-to-day transactions) or complex algorithms such as dapps and smart contracts, according to Volkov.

“Halving the Bitcoin mining reward would likely increase the transaction cost for end-users, so it would give even less motivation to use Bitcoin for small transactions. There is stable, slowly increasing interest from regulators and big investors, so in the long term, Bitcoin will look more like an investment instrument and less like money,” he added.

Polemitis expressed the same sentiment, suggesting that Bitcoin is likely destined to become a store of value rather than a medium of exchange.

"The scaling debate on BTC is over for now."

Antonis Polemitis

“The scaling debate on BTC is over for now," he told Decrypt. "Layer 1 is going to be small blocks and without a huge amount of transaction volume. There is a form of stability right now between the capacity of Level 1—relatively limited for high volume transactions—and demand for high volume transactions; also relatively limited, given the current orientation of BTC to ‘store of value’.”

What could the future hold for Bitcoin?

While it is nigh-impossible to predict how the blockchain could change even in the foreseeable future—let alone in 20 years, given the pace at which digital technologies are being developed today—the experts unanimously agreed that Bitcoin is likely primed to take center stage in the evolution of the finance industry.

“If I had to guess, and this is obviously nothing more than a guess because 20 years is a lifetime in this field, a success case for BTC in 20 years is that it is the global open settlement layer for both a large number of DeFi services and the machine-to-machine economy,” Polemitis asserted.

At present, there is a long list of technical improvements and new features that could be implemented in the Bitcoin blockchain, Volkov added. However, he noted that reaching a consensus on those changes requires too much effort—all while more convenient alternatives already exist today.

“The future of Lightning remains undefined: it was anticipated to be a good technical improvement, but it is still not widely used, is not easy to use, and has many better alternatives now, plus technically Lightning is still not fully ready. So we do not expect any major technical updates on the Bitcoin blockchain in the next few years,” he surmised.

Likewise, Ali suggested that Bitcoin will become “the center of gravity” for the whole cryptosphere in the future.

“In 20 years, I think Bitcoin will be the center of gravity for the cryptoasset ecosystem and broadly the Internet. Think of Bitcoin being as pervasive as TCP/IP, a value settlement protocol that is a reserve currency for the world and a record of hashes of internet data and logic,” said Ali.

According to him, various decentralized finance (DeFi) applications, new types of derivatives and stable currencies will likely be built on top of Bitcoin. Simultaneously, private and confidential transactions would be enabled on top of Bitcoin’s base layer.

“Currently, the finance industry is rapidly adopting cryptoassets like Bitcoin. Soon, the migration will come full circle, and Bitcoin plus connected/side chains will become the new infrastructure that fintech and banks run on top of,” Ali concluded.

Bitwise's Plan to Become the S&P 500 of the Bitcoin Space

Bitwise recently launched America’s first publicly traded crypto index, and CIO Matthew Hougan is optimistic about the future of Bitcoin.

In brief

Bitwise recently launched the first publicly traded crypto index in America.

CIO Matthew Hougan is optimistic about crypto's future.

The goal is to introduce America's wealth managers to crypto.

Bitwise’s 10 Crypto Index Fund went live on December 10, making history as the first publicly traded crypto index fund in the US.

This year has been a big year for Bitcoin’s retail and institutional investors. Companies like Coinbase and Fidelity cater to these groups respectively, but there’s a middle ground of wealth managers—people who manage the wealth of millions of Americans—waiting to be tapped into. Bitwise’s fund is designed to expose these millions of Americans to crypto via their investment portfolios.

“The idea is to be the S&P 500 or the FTSE 100 of the crypto space,” Bitwise CIO Matthew Hougan told Decrypt.

The fund has already enjoyed some success. According to yesterday’s figures, the company is already looking after $162 million worth of assets and trading volume is hovering at just under $100 million.

Bitcoin's price is booming. Image: Shutterstock

Hougan has identified this wealth management space as an untapped, but major area of promise for the cryptocurrency space. “In the US it’s about a $15 trillion market, it’s a market that’s aggressively moving towards crypto at this very moment, and that’s what our products are designed to serve,” Hougan added.

But the road has been paved with several obstacles, not only from America’s regulators, but also from the cryptocurrency industry itself.

Getting regulators to understand Bitcoin

Hougan hopes for Bitwise to push through America’s first Bitcoin Exchange Traded Fund (ETF), where crypto assets are traded on a stock exchange.

“People who get frustrated about ETF progress have to remember that in 2013 or whatever, the largest exchange in crypto was a former site that teenagers used to trade magic gathering cards,” Hougan said, adding that, “It’s not like we were born into a highly regulatory existence.”

That fact, in turn, gives Hougan some understanding about the perspective of an SEC regulator facing the concept of an ETF for cryptocurrencies.

“The point they’re starting from, is that Bitcoin is this crazy anarchic market run on exchanges like Mt. Gox that collapse and people lose all their money,” he said.

Moving the SEC from that starting point to a point where a crypto ETF would be authorized in the United States might sound like a long road, but Hougan is not dissuaded. “The market is maturing, it’s getting more institutional, we’re going to get an ETF.”

And for Hougan, waiting on the regulators will be worth it in the long run.

But while previous comparisons between Bitcoin and gold have led to excitement in the crypto space, for Hougan—precisely because Bitcoin is following a trail paved by gold—the excitement generated by Bitcoin will one day come to an end.

“I think we’re going to advance to a future where Bitcoin is as boring as dirt,” Hougan said, likening Bitcoin’s path to that of gold fifty years ago, when, like Bitcoin, gold was volatile.

“[Gold] exited the 1970s with a 1,300% return and a 600% real return, it wasn’t just keeping place with inflation, it sort of doubled nominal inflation over that period,” he added. In other words, for Hougan, Bitcoin is figuring out its place in the world today, much like how gold had to figure out its own role after the gold standard era.

And in its hunt for a seat at the table, Bitcoin can only benefit from an ever-growing list of institutional investors that grant the cryptocurrency greater perceptions of legitimacy. One such example is MassMutual, a stalwart of America’ insurance industry that is now embracing Bitcoin.

“MassMutual was formed when Millard Fillmore was the President in the US in 1851, and now they own $100 million in Bitcoin,” Hougan said.

Bitwise Investments. Image: Bitwise

And, precisely because Bitcoin has changed so much over the years, it’s to be expected—even praised—that people have changed their views.

“In the early days of Bitcoin, its probability of success was extremely low, and it’s now supported by the largest super computing network in the world, it’s not clear that any sovereign non-economic actor could disrupt it, it’s got a ten year track record,” Hougan said.

But this doesn’t mean Bitcoin is home free. For one, Hougan believes the potential spoiler to Bitcoin’s lucrative future is a bug in the code. Or, potentially, an attack on Bitcoin’s codebase.

“That bug could be latent, or it could be introduced in an upgrade, it’s not like the code is fixed in stone,” Hougan said, adding “Someone without economic self-interest—like a government actor attempting to disrupt it—is a possibility.”

Hougan did clarify that he thinks such an attack is unlikely, but emphasized there is never total certainty. In any case, he added that there is plenty of cause for optimism about the future of cryptocurrencies.

“The biggest risk in crypto investing is behavioural: people buying high and selling low,” Hougan said, adding that the introduction of financial advisors could “lead to better behavioural outcomes, and I think that will benefit the asset class.”

MTI — Grow your Bitcoin Daily by automation. 270,000 Members

Grow Your Bitcoin Daily! MIRROR TRADING We are a Copy Trading Service that launched in April, 2019 CEO Johan Steynberg from South Africa Trading reports shown by License Broker called FX Choice â

Get Paid 5 Days a Week except Weekends â

Paying 10 to 12% per Month â

Profits automatically Compounded â

Daily Trading Reports via Email and the Backoffice â

Min $100 Investing

Min $200 to earn to Binary 10 Levels â

10% Referrals â

NO Withdrawal Fees â

Withdraw Capital anytime FREE MEMBERS please note : A minimum investment of $100 in bitcoin is required. A minimum of $200 in bitcoin should you want to participate in earning Weekly Residual Binary Bonuses Those FREE MEMBERS who have not funded within the 7 days — their accounts will be closed and removed during Daily Binary Compression. Re-registration is permitted.

The new account will be placed in the next open binary position.

P.S *MTI Opportunity Overview* Our corporate presentation team works hard to bring you the best quality, most insightful view of our MTI opportunity. Join us for a look at what MTI has in offer! Calls are scheduled everyday, *Monday to Friday* 10am, 3pm and 7pm (South Africa)

8am, 1pm and 5pm (Ghana/Liberia)

9am, 2pm and 6pm (Nigeria/UK)

4am, 9am, 1pm EST (USA)

1:30pm, 6:30pm and 10:30pm India

12am, 4am and 7pm (Australia)

12pm, 5pm and 9pm (Dubai)

A variety of seasoned presenters and trainers will do a meeting covering the full MTI opportunity.

Ethereum DeFi Token Plunges From $1.5M Market Cap to $15K

DistX's founders left the project and the price quickly collapsed. But not before some last-minute transactions.

In brief

DistX was a token sale platform.

When founders left the project, the price fell to practically $0.

The protocol deleted its social media accounts shortly thereafter.

Rug pulls and exit scams in decentralized finance have become so ubiquitous that they're hard to keep up with. Moreover, they're often accompanied by assurances that this is not, in fact, part of a scam.

The most recent suspected rug pull—when a project team works to increase market cap then suddenly steps away and cashes out, leaving investors holding the bags—is DistX.

The token has sunk to a market cap of $15,000 after enjoying a cap of over $1.5 million just yesterday.

DistX, not to be confused with district0x, billed itself as a token sale platform. DistX token holders were promised not only access to tokens launched on the platform but also, if they held enough of the tokens, a 2% share from the sales.

After becoming available in August, the token hit a high of $0.25 before settling into the 6-8 cent range over the last month.

And then the bottom dropped out over the weekend, with the price plummeting to next to nothing. The market cap, which was $1.5 million on December 14, went all the way to $8,670 and now sits at $15,000, according to data from CoinGecko.

DistX price. Source: CoinGecko

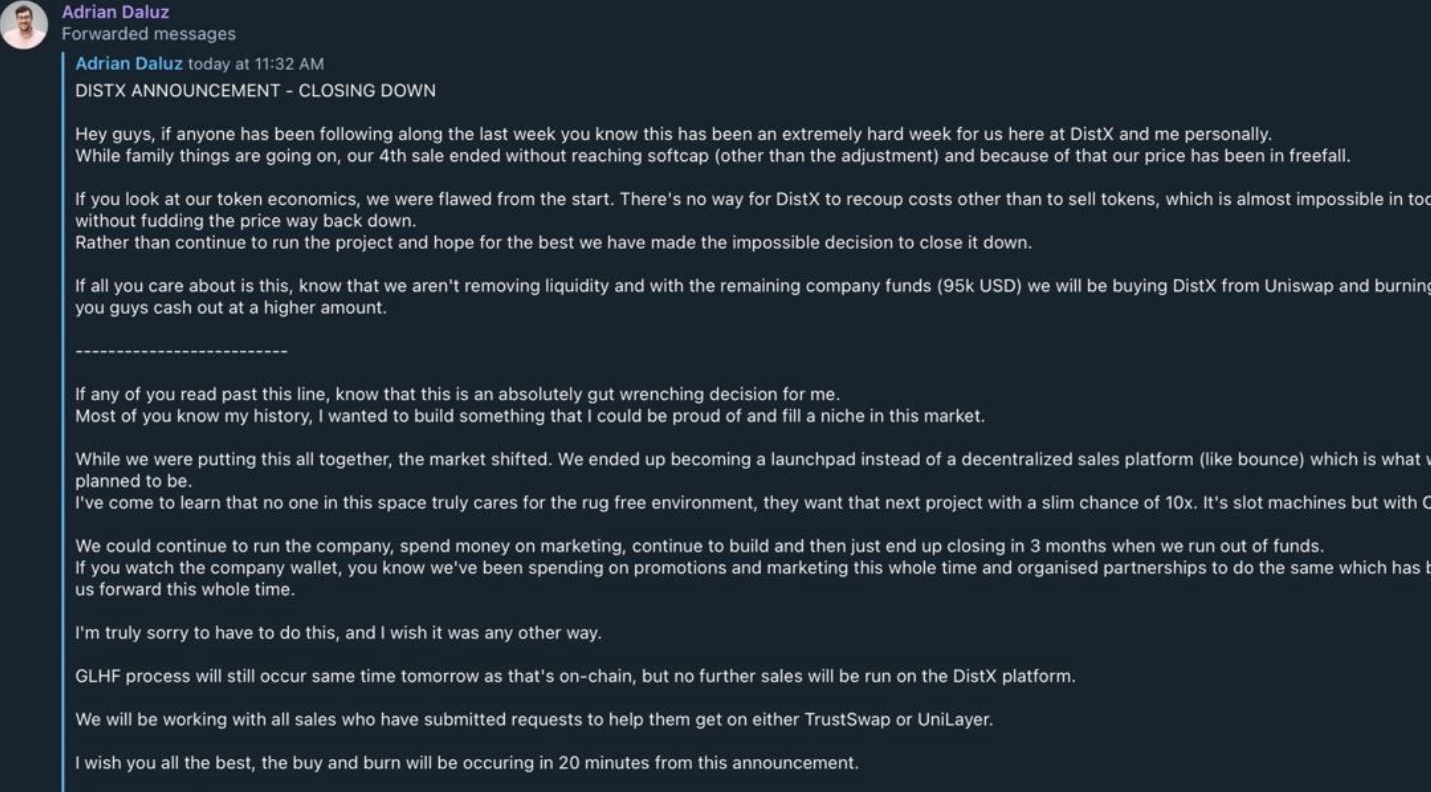

As originally reported by CryptoSlate, a project founder, Adrian Daluz, announced on Sunday, December 13, that, after DistX's fourth token sale failed, they'd be closing down.

However, Daluz added:

“If all you care about is this, know that we aren’t removing liquidity and with the remaining company funds (95k USD) we will be buying DistX from Uniswap and burning it to help you guys cash out at a higher amount.”

Parting message from Adrian Daluz. Source: WARONRUGS

Those reassurances were undercut by severaltransfers of over 192 Ether (worth $112,000) that appear to have removed that liquidity from Uniswap, according to WARONRUGS, an anti-scam group.

But Jeff Kerdeikis, CEO of token launchpad TrustSwap (which is not affiliated with DistX) said he was working with DistX to figure out a way to salvage value for token holders:

Daluz and DistX were unavailable for comment as their social media accounts had been deleted. Comments on the Telegram group have been muted. Not good signs. Decrypt reached out to Kirdeikis to inquire about the nature of the discussions with DistX but has not yet received a response.

DeFi has suffered from a rash of rug pulls and exit scams as the market heats up and everyday investors try to get in. It's also witnessed plenty of projects fail or slowly fizzle out.

DistX holders at the moment, however, likely don't care too much about the reasons for the abrupt exit. They just want the token they bought to be worth north of nothing.

Bitcoin Lovin’ Senator Hires ‘Crypto Cowboy’ as Wyoming Policy Director

Cynthia Lummis and Tyler Lindholm are bringing Bitcoin to Washington.

In brief

"Crypto Cowboy" Tyler Lindholm is joining Cynthia Lummis's senior staff.

Lummis just won a US Senate seat, the first woman from Wyoming to do so.

Both Lummis and Lindholm are big fans of Bitcoin.

Cynthia Lummis, the incoming Republican Senator who’ll bring Bitcoin to the US Congress, has hired Tyler Lindholm, Wyoming's “Crypto Cowboy” as the State Policy Director of Wyoming.

Lindholm, who is also Chief of Ranching Operations at BeefChain, a food chain supply company that promises “blockchain verified beef & sheep,” will begin his new job on January 3, 2021, a little under two weeks before President-elect Joe Biden’s inauguration.

Lindholm, formerly Wyoming State Representative and co-chair of the Wyoming Blockchain Task Force, passed several pro-crypto pieces of legislation to encourage crypto businesses to the state, among them the Utility Token Act and the Digital assets-existing bill.

Such legislation has helped the state attract big blockchain business. Kraken Financial, the banking arm of crypto exchange Kraken, won a license from Wyoming to set up the nation's first crypto bank. IOHK, the creators of Cardano, opened a blockchain lab at the University of Wyoming.

Lummis, a native of Wyoming and an alumna of the state’s university, told podcaster Peter McCormack in a podcast published today, and recorded on December 1, “I really want to use my time in the US Senate, in part, to help introduce the topic of Bitcoin, increasing the understanding in the Senate about Bitcoin.”

“What it is, what it does, how it can be an asset that can grow and develop as an adjunct, or basically alongside, fiat currency.”

Bitcoin, said the conservative Senator, feels like an American idea. In her campaign for Senator, Lummis pushed for an “America First” policy.

“Bitcoin can function alongside a fiat currency and adjunct store of value; in fact, a better store of value than a fiat currency,” she told McCormack.

If anything, Bitcoin could do an even better job than the meddlin’ Fed, she sniffed. “In the case of US currency, inflation is baked into the Federal Reserve's plan for the US dollar. So it's no wonder that our buying power is eroded,” she said.

Other things on Lummis’s to-do list during her time in the Senate include building a wall on the southern border of the USA, defending the second amendment and stopping the “socialist agenda.” Her new commander-in-chief may not approve.

Bitcoin’s "Realized" Price Hits Another All-Time High

Bitcoin’s metrics are looking good: its “realized” price and cap today hit new highs.

In brief

As Bitcoin’s current price rises, so does its “realized” price.

Today its “realized” price hit an all-time high of $7,670.15.

Bitcoin’s “realized” cap also hit a new all-time high.

Bitcoin’s price is on the up—but that’s not the only metric breaking records.

Today, Bitcoin’s “realized” price hit an all-time high of $7,670.15, according to data metrics site Glassnode.

“Realized” price is different to the actual price in that it refers to the value of coins that are actively used. It monitors the value of active cryptocurrency—and excludes lost coins or cryptocurrencies left dormant in wallets for years.

It is calculated by dividing the “realized” capitalization by the circulating supply.

And today, Bitcoin’s “realized” capitalization also hit an all-time high of $142.43 billion, Glassnode announced.

This metric, devised by analytics firm Coin Metrics, measures the aggregate value of a cryptocurrency network by multiplying each cryptocurrency by the last time it moved.

So if a coin last moved in 2018 when the price was $4,000, the metric takes that price into account, rather than today’s price, when calculating the “realized” cap.

These new all-time highs are indicative of a healthy market: Bitcoin’s price has smashed records this year as an explosion of interest in the crypto-world—particularly decentralized finance—and interest from institutional investors has led more people to invest in the currency.

Bitcoin’s current price today pushed past the $19k mark, hitting $19,171—an increase of 4.42% in the past 24 hours—according to CoinMarketCap data.

To have a competitive Online Business in today's world, Social Media Marketing needs to be part of your Marketing Strategy. Below are procedures to create an effective plan for growing your business and your bottom line.

Before we start, though, let's define just what is a Social Media Marketing strategy.

What is a social media marketing strategy?

Following are some questions that need to be addressed when creating a Social Media Strategy:

What are the Objectives: what are the results you're looking for, and how will they be measured?

What is the Target audience: outline the characteristics of your ideal customer.

What will be your Content Mix: put together a social media schedule based on your recurring presentation formats.

Which Channels you will select: what will be the best of the social networks available to use, and how will you use them.

What is your Process: outline the procedures and tools used to execute your strategy effectively.

Answering these questions will produce a framework for laying the foundation of your Social Media Strategy and better prepare you for knowing how to combine them and review your strategies progress over time.

Step 1. The Why

Identify your reason to begin marketing on social networks. Why provide business access to your social media and SME? If you only wish to place ads and sell by sending targeted messages, this strategy is not for you.

Social networks are conversations. Consumers want to converse, criticize, report, and advise the company or brand name of their experience or if they have a complaint about a product or service.

So be clear about your goals and objectives on social media. Do you want to retain and talk with existing customers, build your brand reputation, or find new customers and increase sales? Each of these objectives determines how your business behaves on social media and in which networks you should participate.

Important: List out the main reasons why you want to get started on social networks. Be specific about the results you are looking to achieve (clear objectives: quantity and goals).

Step 2. The Plan And Other Marketing Aspects

When you put together your online plan, think about how social networks will be integrated into the company's overall digital marketing plan. Will you be selling through social media? Would you be using Twitter, for example, to make offers? How will you determine the success of your efforts, both online and offline?

Important: If, for example, the customer service or sales team is affected by the new social marketing tools, be sure to take the time to bring them up to date. Make sure everyone has the same goal for both in-house and outside communication.

Step 3. Communicating: Defining Your Voice

How will your product be offered online, and who is in charge of communication? Will it be a company director, the owner, an employee, or perhaps an outside advisor? Frequently, companies manage a presence with several individuals who share duties. On social network platforms, you must express your brand value. No one will render your presence necessary, not having your own defined value.

Important: Based on your business's size, it requires investing insight, time, and capital to plan with your marketing partners how your organization is presented, how it communicates, and who manages it.

Step 4. Define Your Customer

Identify who makes up your target audience? Where are they located? What gender and age are they? In a physical store or business, you can connect with your customers. Online, however, you should investigate where they spend time. This includes both learning and listening online. One example, for local businesses, Facebook may provide more influence than LinkedIn.

Social media is worldwide. Are you conversing with everyone just concentrating on your local customer base? Invest your time outlining your contact strategy for your social media target audience.

Important: Who are they? Where are they? And any additional info regarding your target audience will assist you in creating a successful marketing strategy and better segment your customer base.

Step 5. Examine And Evaluate Everything

How will "influence" on social media be determined? Some methods are measured by sales. Others could be based on fulfilling customer requests, creating a brand, prompting questions, or building email lists.

Each of these measures is valid. Specify your goals before beginning, so you can plan out, evaluate, and determine if your endeavors are successful.

Important: Select some metrics and create a simple way to track and evaluate them, such as a spreadsheet that indicates the increase of fans weekly. Whether or not the investment for analysis and measurement is profitable will be shown in the medium term.

Hopefully, this guide will help beginners in social networking start more cleanly and in a planned way. It can help to ensure the success of your business in a reasonable time.

Markethive — The Perfect Complement

The perfect complement for your Social Media Marketing or any marketing you want to do isMarkethive. They deliver an Inbound Marketing platform equal to or superior to Marketo and Hubspot.

Markethive’s tools include email autoresponders, blogging platforms, landing pages, social media broadcasting, Tracking analytics, SEO, backlinking automation, messaging, and e-commerce.

The benefits of these systems are to "attract and engage," "convert and nurture," "close and delight," "analyze" and build a large, loyal, long-term customer base.

For any additional information or to become a Free Member, Click on the Banner below:

Written byGene Aasen

Entrepreneur 1 and Writer for Markethive.com, the social, market, broadcasting network. I’m a strong advocate of the Markethive mission for technology, world progress, and freedom of speech. I support change and endeavor to help others understand, grow, and move forward with enthusiasm to achieve their goals.

MTI — Create Passive Residual Income Wealth Daily with Bitcoin

Grow Your Bitcoin Daily! MIRROR TRADING We are a Copy Trading Service that launched in April, 2019 CEO Johan Steynberg from South Africa Trading reports shown by License Broker called FX Choice â

Get Paid 5 Days a Week except Weekends â

Paying 10 to 12% per Month â

Profits automatically Compounded â

Daily Trading Reports via Email and the Backoffice â

Min $100 Investing

Min $200 to earn to Binary 10 Levels â

10% Referrals â

NO Withdrawal Fees â

Withdraw Capital anytime FREE MEMBERS please note : A minimum investment of $100 in bitcoin is required. A minimum of $200 in bitcoin should you want to participate in earning Weekly Residual Binary Bonuses Those FREE MEMBERS who have not funded within the 7 days — their accounts will be closed and removed during Daily Binary Compression. Re-registration is permitted.

The new account will be placed in the next open binary position.

P.S *MTI Opportunity Overview* Our corporate presentation team works hard to bring you the best quality, most insightful view of our MTI opportunity. Join us for a look at what MTI has in offer! Calls are scheduled everyday, *Monday to Friday* 10am, 3pm and 7pm (South Africa)

8am, 1pm and 5pm (Ghana/Liberia)

9am, 2pm and 6pm (Nigeria/UK)

4am, 9am, 1pm EST (USA)

1:30pm, 6:30pm and 10:30pm India

12am, 4am and 7pm (Australia)

12pm, 5pm and 9pm (Dubai)

A variety of seasoned presenters and trainers will do a meeting covering the full MTI opportunity.

Ethereum’s Vitalik Buterin Says We Need to Talk About Wallet Security

We aren’t talking about making things more secure in the crypto world, says Ethereum’s co-founder. And user-friendly wallets are a must.

In brief

Ethereum co-founder Vitalik Buterin today spoke at the Latin American Bitcoin Conference.

He said wallet security is one of the biggest issues in the crypto space.

Buterin added that Ethereum 2.0 was making “massive progress.”

Ethereum 2.0 is coming—in fact, Phase 0 is already here—potentially bringing with it loads of new users and use cases. But it’s going to be all for naught if we don’t solve a deeply unsexy issue: wallet security.

Ethereum co-founder Vitalik Buterin said at the Latin American Bitcoin Conference today that the fact wallets are still too difficult to use, making them somewhat insecure for non-technical users, could prove troublesome when mass crypto adoption actually happens. Worse, it could even lead to people “gravitating to centralized solutions.”

When asked what issues weren't given enough focus in the industry, Buterin replied, “The security side—wallet security. It’s still much easier than it should be to lose $200,000 if your wallet breaks. I have a theory that we don’t talk about the problem enough because no one is willing to admit they lost $200,000 because if you admit you lost $200,000, you look like an idiot.

“No one talks about it so people think the problem is small when there are lots of cases everywhere.”

He added: “I think the reality is that even if you are a super genius or capable of being really careful, the reality is a system that requires you to expand less effort on not losing your stuff is a better system.”

Moving on from the topic that most people aren’t talking about to the event that has people abuzz, Buterin said that Ethereum 2.0 (Eth 2) was helping to solve problems in regards to privacy and scalability. Eth2 is an upgrade to the Ethereum network meant to increase the blockchain’s transaction capacity and lower transaction costs.

Ethereum’s network was pushed to its limit this year when decentralized finance (DeFi) applications—which are nearly all built on Ethereum—became hugely popular. The Eth2 upgrade will allow the network to run with ease as it gradually attracts more users.

Buterin said that Eth2 “unlocks huge amounts of possibilities” and that the network could “theoretically handle 3,000 transactions per second”—when that many people are actually using the network.

Ethereum 2.0 won’t be functional for a while yet: hopefully that’ll give developers enough time to figure things out. As Buterin said, “more attention on minimizing risks and maximizing opportunities” should come first.